- The ZorroFi Update

- Posts

- The Lending Brief - October 21

The Lending Brief - October 21

Sandra Wasicek

October 21, 2025

Welcome to The Lending Brief,

This is your weekly update on what’s breaking (and fixing) modern lending.

On October 17, Zions disclosed $60M in loans with “apparent misrepresentations,” expecting to lose $50M after recovery. That single disclosure wiped $1B off regional-bank valuations.

As one senior banker put it: “Fraud can go on for years before it’s uncovered.”

That’s exactly what happened - and why investors are suddenly asking how banks verify collateral when the borrower is lending to someone else.

👉 Do you lend to auto dealers, equipment lessors, or lenders-to-lenders? Keep reading.

Insight 1: “When You See One Cockroach …”

“When you see one cockroach, there are probably more.” - Jamie Dimon, JPMorgan Chase

Zions’ $50 million charge-off over “apparent misrepresentations” sparked a billion-dollar sell-off. The exposure was small; the reaction was psychological.

The irony: NDFI loans report the lowest delinquency rate among major categories -just 0.10% non-performing as of Q2 2025. Yet when fraud appears, investors panic because they can’t see the collateral. One case shakes confidence in them all. In fact, NDFI lending concerns became the topic du jour of third-quarter earnings calls across the industry.

What actually happened:

Each case exposed the same weakness - collateral opacity. Banks leaned on borrower representations and legacy document reviews built for slower times. By the time missing liens or double-pledged assets surfaced, the market had already priced in distrust.

Fraud used to be a compliance issue. Today it's a confidence signal. In Zions' case, the $1 billion market selloff cost 20× more than the $50 million loan loss.

The Cantor Group case shows how: forged title insurance, undisclosed lien subordination, and property transfers through shell entities - undetected for years. Lawsuits now involve Zions ($50 M), Western Alliance ($99 M), and three others.

⚡ Action Step:

When examiners ask, “How do you verify collateral between annual reviews?” - what’s your answer? If it’s “We don’t” or “Borrower tells us,” that’s your blind spot.

🔍 Want to know more?

CNBC’s Leslie Picker explains why fraud recoveries are often worse than bankruptcies—because there’s nothing left to seize. (2 min watch)

Insight 2: The NDFI Blind Spot

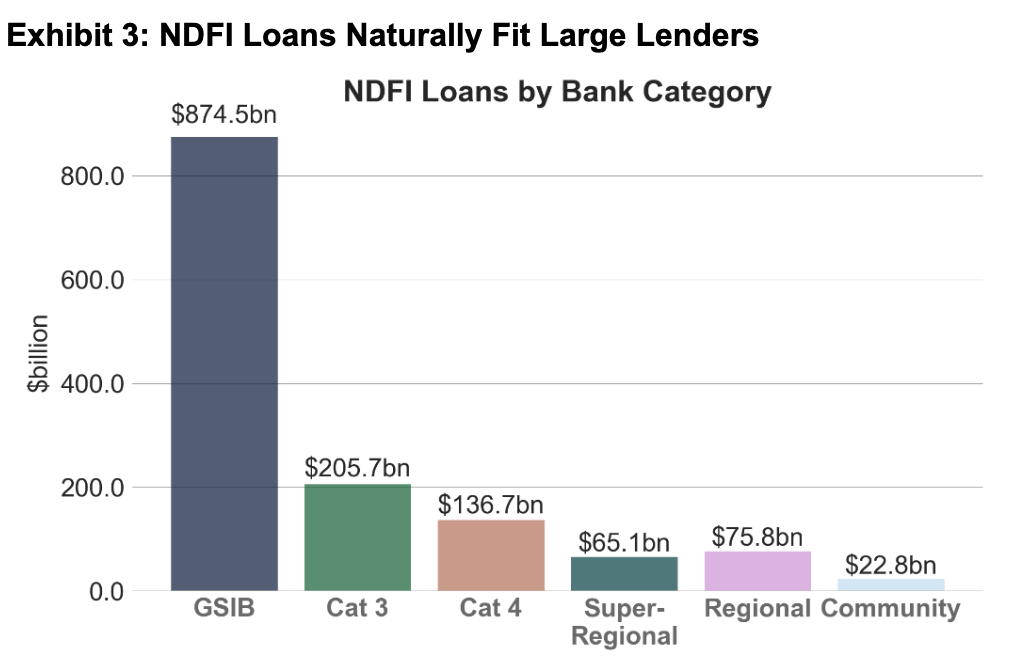

The 2025 FDIC Risk Review flags non-depository financial institutions (NDFIs) as the fastest-growing loan category - up 30% last year to over $1 trillion.

What are NDFIs?

NDFIs make loans but don't take deposits: auto-finance companies, equipment lessors, mortgage brokers, fintech lenders. Banks and credit unions fund them through floor plan financing, equipment lines, and short-term credit for mortgage brokers and fintechs — and that one layer of separation hides the collateral.

Where the risk sits

After 2008, risk migrated outside the regulated perimeter. Today, many institutions finance lenders whose books aren’t visible in real time. Collateral may be over-valued, re-pledged, or fictional.

For institutions under $10B in assets, NDFI lending as a percentage of Tier 1 capital grew from 1% to 5% (2010–2024). If you finance dealer floor plans, equipment leasing lines, or provide short-term credit to mortgage brokers or fintechs, you're exposed.

Cantor Group was an NDFI funding distressed real estate through bank credit lines. Its shell-entity structure showed how complexity masks risk: different sector, same problem - loans secured by collateral nobody verified.

Why does it matter to lenders?

FDIC: “Assessing credit decisions of nonbanks is particularly difficult.” Translation: you’re lending against assets you can’t see, managed by entities you don’t supervise. Examiners won’t ask if the borrower lied - they’ll ask how you verified the collateral.

As Truist Securities analyst Brian Foran put it: “What we know looks good - but you don’t know what you don’t know.”

⚡ Action Step:

List every loan where you lend to a lender. For each, document three fields:

• Who reports collateral value

• How you independently verify it

• How often it happens

If any answer is “annual audit”—that’s your gap.

🤝 Insight 3: Relationships Win When They’re Verified

A community-bank CEO told us: “We curate our relationships. That’s what sets us apart.” He’s right - relationship banking remains the edge.

Even Robinhood’s Vlad Tenev told attendees at the Fed’s Community Bank Conference: Digital-only platforms can’t replicate local trust. But he also acknowledged AI can spot fraud patterns humans miss. Both are true: relationships build loyalty; verification protects it.

The Zions case proved it. A longstanding relationship - and fraud that slipped through because verification happened only at origination and renewal. By the time another bank’s lawsuit surfaced the pattern, the damage was done.

Fifth Third's Chief Credit Officer put it plainly: they launched an “end-to-end inspection of processes, policies, underwriting and portfolio monitoring” - and found gaps to close.

⚡ Action Steps:

1️⃣ For new loans: Who verifies documents are legitimate? If the answer is "we review what borrowers upload," that's not verification - that's trust.

2️⃣ Pick one recent loan. Trace the verification: Who confirmed the data independently? If no one did, you're lending on borrower representations.

3️⃣ Ask your team: What fraud red flags do we screen for at intake? If the answer is "credit score and income," you're missing behavioral signals and document manipulation.

🦊 ZorroFi insight

Fraud doesn't start with fake borrowers - it starts with unverified data. When lenders rely on borrower-supplied files instead of validating key facts at the source, small errors become booked exposure.

The Cantor case proves it: long-standing relationships can hide systemic fraud when intake depends on paperwork, not proof. Whether it’s commercial real estate or SMB credit, verification at the source stops fraud before it books.

Modern intake isn’t about collecting forms - it’s about confirming facts. The edge isn’t stricter checks; it’s confident, verifiable decisions that protect relationships and reputations.

💡 Want to Dive Deeper?

Demo: I work with CDFIs, community banks, and credit unions on modernizing lending. Reach out for a short demo.

Subscribe: Get the full breakdown every Thursday in my LinkedIn newsletter -Lending Insights.

Watch: Bloomberg’s Chris Whalen on private-credit opacity and why banks must verify what they can’t see (5min)

🙌 Help Us Grow

Know someone in lending who’d benefit from these insights? Forward this email — and hit reply if there’s a topic you’d like us to explore next.

📅 Next newsletter drops Tuesday, 10/28.

| Warmly, |